At the beginning of 2025, China's manufacturing production maintained growth for the fifteenth consecutive month, with the growth rate surpassing that of December 2024. New orders showed a similar trend. According to surveyed sample enterprises, the improvement in basic demand during the month, coupled with promotional efforts by enterprises, drove an increase in new orders, supporting production expansion……

- CPCA: Retail Sales in the Passenger Vehicle Market Reached 2.2 Million Units in January 2025, Down 12.1% YoY

The CPCA released the latest sales data. In January, retail sales in the national passenger vehicle market totaled 1.794 million units, down 12.1% YoY and 31.9% MoM. January retail sales were at a historically low level, with the MoM decline of 31.9% being second only to the 41% drop in January 2023.

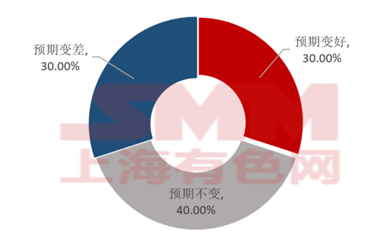

The significant decline in overall vehicle sales in January 2025 was mainly due to the impact of the Chinese New Year holiday, which shortened the effective sales period, along with demand overdraft caused by automakers' inventory pressure at the end of 2024. Among the automakers surveyed by SMM, 30% reported an improvement in new orders MoM in January, 30% indicated that orders remained stable compared to December, while the remaining 40% reported a decline in orders MoM. One automaker mentioned, "Sales orders are concentrated overseas, and the overseas market is the focus this year. Domestic orders are not performing well, just like last year."

Figure 1: January Order Status of Sample Automakers Surveyed by SMM

Regarding the order outlook for the next three months, among the automakers surveyed by SMM, 30% held a positive view, 30% held a negative view, and the majority (40%) expected no change in demand. This is mainly because most of January and February are spent on holiday during the Chinese New Year, which may lead to a decline in operating rates, while order-taking remains basically stable.

Figure 2: Three-Month Demand Outlook of Sample Automakers Surveyed by SMM

- ChinaIOL Data: January 2024 Air Conditioner, Refrigerator, and Washing Machine Production Up 38.3% YoY

According to the production report on the three major white goods released by ChinaIOL, the total production of air conditioners, refrigerators, and washing machines in January 2024 reached 29.93 million units, up 38.3% YoY, achieving a "good start." Specifically, household air conditioner production in January was 16.29 million units, up 53.2% YoY; refrigerator production was 7.15 million units, up 48.8% YoY; and washing machine production was 6.49 million units, up 4.6% YoY.

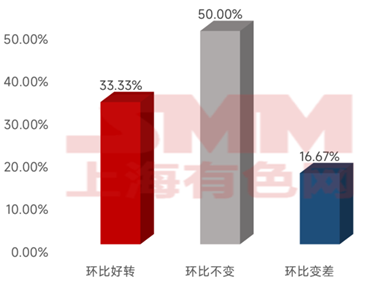

In January 2024, the home appliance sector showed positive production and sales performance at the beginning of the year. Air conditioner exports maintained high prosperity, domestic sales grew well, and refrigerators and washing machines performed relatively steadily, with washing machine domestic sales showing good growth. Among the home appliance enterprises surveyed by SMM, about 33.33% reported an improvement in orders MoM in January, 50% indicated no significant change MoM, and only 16.67% reported a decline MoM. A company in Fujian mentioned, "Currently, we have 2-3 months of orders and inventory on hand. January to April is the peak production season, with sufficient orders and high operating rates. This month, due to the Chinese New Year holiday, the operating rate will decline."

Figure 3: January Order Status of Sample Home Appliance Enterprises Surveyed by SMM

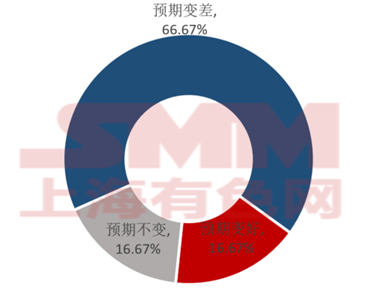

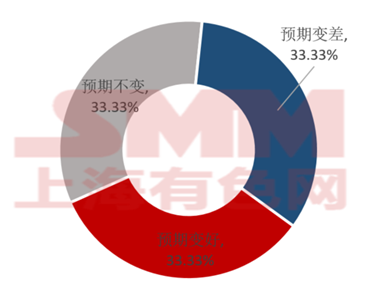

Regarding the order outlook for the next three months, among the sample enterprises surveyed by SMM, nearly 66.67% expected a MoM decline, mainly due to the off-season next month, which will significantly reduce total production and operating rates.

Figure 4: Three-Month Demand Outlook of Sample Home Appliance Enterprises Surveyed by SMM

According to the latest production report on the three major white goods released by ChinaIOL, the total production of air conditioners, refrigerators, and washing machines in February 2025 reached 29.14 million units, up 30.6% YoY. By product, household air conditioner production in February was 15.93 million units, up 35.6% YoY; refrigerator production was 6.32 million units, up 29.2% YoY; and washing machine production was 6.89 million units, up 21.3% YoY.

- China Construction Machinery Association: Excavator Sales Up 1.1% YoY in January 2025

According to statistics from the China Construction Machinery Association, in January 2025, major excavator manufacturers sold 12,512 units of various excavators, up 1.1% YoY. Among them, domestic sales were 5,405 units, down 0.3% YoY, while exports were 7,107 units, up 2.19% YoY.

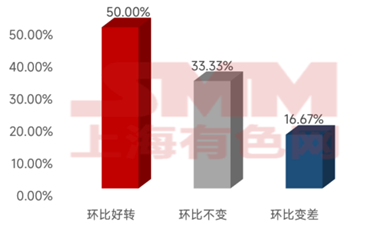

In January 2025, according to SMM survey data, the overall operating rate of the machinery industry was 59.1%, down 7.8% YoY. This month, the operating rate was at a low level due to the Chinese New Year holiday and seasonal factors, but some sub-products still experienced full orders. SMM expects the operating rate of the machinery industry to be about 57.1% in February and about 67.4% in March. Among the machinery enterprises surveyed by SMM, about 50% reported an improvement in orders MoM in January. A machinery enterprise in Xiamen mentioned, "The holiday affects the operating rate, which will drop slightly, but the recent new project intake is quite good. We have taken on some new projects in steel structures and containers. For 2025, the production pace is expected to be relatively normal, around 60-70%."

Figure 5: January Order Status of Sample Machinery Enterprises Surveyed by SMM

Regarding the order outlook for the next three months, among the sample enterprises surveyed by SMM, opinions on the future development of the machinery industry were evenly divided. In 2025, the export chain of the machinery industry will face significant changes in the trade landscape, especially due to the uncertainty of US policies. Trump's tariff policies have become a market focus, with potential tariff hikes posing risks to the global trade landscape and China's machinery industry export chain. However, in the long term, these trade changes also bring new opportunities for China's machinery industry.

Figure 6: Three-Month Demand Outlook of Sample Machinery Enterprises Surveyed by SMM

- Clarksons: New Ship Prices Rose MoM in January 2025, While New Orders Fell 78% YoY

According to Clarksons data, as of the end of January 2025, the Clarksons Newbuilding Price Index stood at 189.38 points, up 0.12% MoM and 4.40% YoY, and up 48.99% since 2021, at the 98.89% historical peak percentile. By ship type, container ship prices rose MoM, while tanker, bulk carrier, and LNG carrier prices slightly declined MoM.

According to the latest Clarksons data, in January 2025, global new ship orders totaled 51 vessels or 1.46 million CGT, down 38% MoM from December 2024's 2.36 million CGT and down 74% YoY from January 2024's 5.59 million CGT. Among them, South Korea secured 13 vessels or 900,000 CGT, accounting for 62% of the market share by CGT, ranking first; China secured 21 vessels or 270,000 CGT, with a market share of 19%, ranking second. As of the end of January, global new ship order backlogs totaled 156.79 million CGT, down 1.32 million CGT MoM. Among them, China's new ship order backlog reached 91.51 million CGT, down 110,000 CGT MoM, up 25.14 million CGT YoY, maintaining the top position with a 58% market share; South Korea's new ship order backlog was 37.02 million CGT, down 880,000 CGT MoM, down 1.91 million CGT YoY, ranking second with a 24% market share.

*[Survey Method: Telephone Survey]

*[Sample data is randomly collected nationwide, covering industries such as automobile manufacturing, home appliances, machinery, and shipbuilding, with a total of over 100 samples. The limited sample size may lead to deviations from actual conditions, so please refer with caution.]

![The most-traded BC copper contract closed down 2.85%, as speculative fervor cooled, weighing on copper prices [SMM BC Copper Review]](https://imgqn.smm.cn/usercenter/CYktX20251217171711.jpg)

![The Black Industrial Chain Lacked Upward or Downward Momentum Before the Holiday [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/FRcmT20251217171746.jpg)

![The most-traded SHFE tin contract plummeted more than 8% in a single day, and tin prices are expected to remain in the doldrums in the short term [SMM Tin Futures Review]](https://imgqn.smm.cn/usercenter/LLUUJ20251217171751.jpeg)